本文來自:致我們深愛的債券市場,作者:楊爲斆

摘要

1、與典型的牛市狀態不同的是:機構交易在這一輪利率下行過程中的貢獻莫大,長期國債的交易量佔比已達歷史次高。

2、長端品種被大幅交易的原因可能有二:

1)天生偏好交易長債的非銀機構的負債端大幅擴張,資金在不斷向廣義基金集中;

2)廣義基金也在積極加久期,公募基金的久期已經升到了歷史最高的位置(4.5Y)。

3、資金被擠向長債資產的緣由是資產荒,這與2016年的環境非常相似:

1)在地產及基建的產業政策層層約束下,有很多資金進不到實體層面之中,只能進入阻力更小的金融市場;

2)權益資產這類中高風險資產的確在今年面臨着比以往更高的風險,大量資金只能在長端債券上尋找一些相對合適的風險收益比。

4、這種交易結構本身就意味着利率債的風險:

1)市場過多交易長端債券本身就意味着行情的不穩定,擁擠的交易通道重新出現;

2)如果將公募基金久期看作公募基金對未來行情的樂觀程度的話,那當前的久期顯示:公募基金的情緒已經出現了不可思議的高漲。

5、我們要警惕利率這個資產之錨出現意外飆升,大類資產的risk-off趨勢尚未坐實:

1)我們需要認清的是:全球的基本面並未出現非常明顯的下降,加之利率被明顯低估的事實,利率其實是易上難下的;

2)當溫水沸騰之時,不但意味着利率債的風險還將延續,也意味着中高風險資產在明年的表現可能要比預期情形更弱一些。

風險提示:貨幣政策超預期,經濟復甦超預期

正文

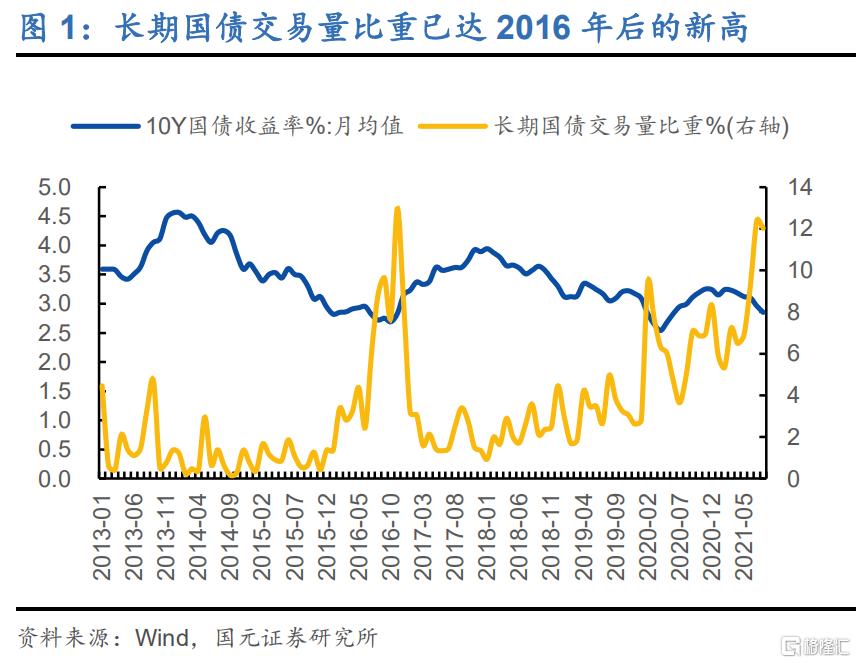

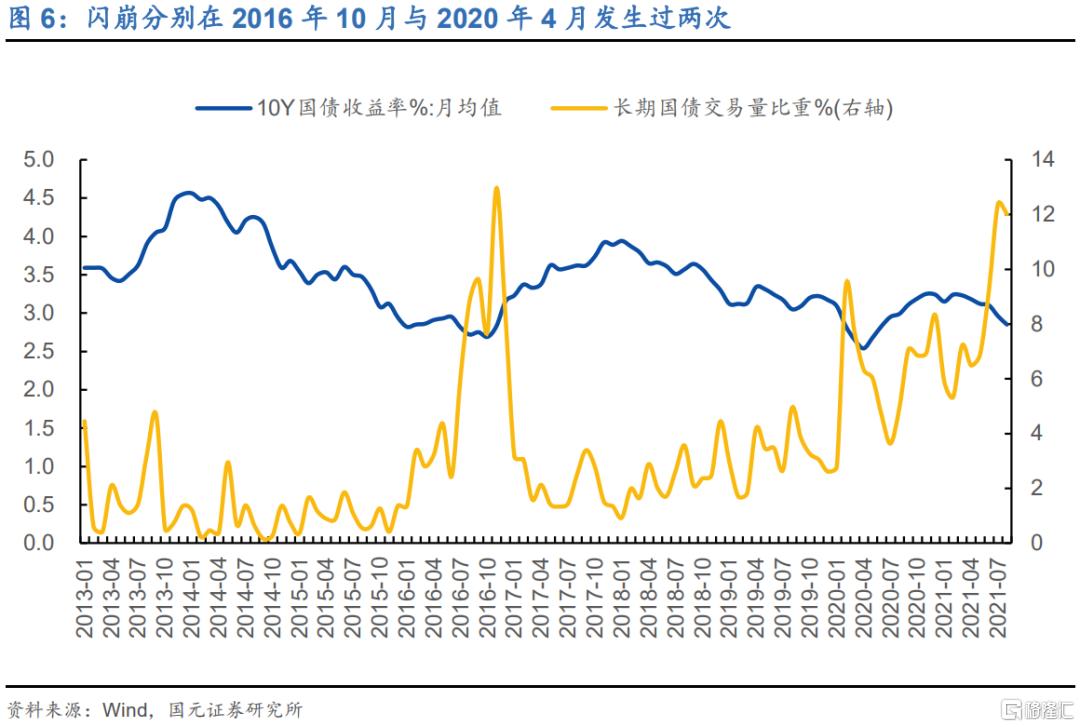

當前交易層面所顯示的信號是:當前的收益率下行只是資金持續交易長端的結果,並非典型的牛市結構。截至目前,長期國債的交易量的佔比已經高達12%,這是2016年債券市場瘋狂加槓桿後的新高水平。這意味着:這一輪收益率的下行很可能是被長端收益率而非短端收益率壓下來的,一個跡象是:當前的期限利差非常穩定,這也同樣說明機構交易在這一輪利率下行過程中的貢獻莫大。

長端品種被大幅交易的原因可能有二:

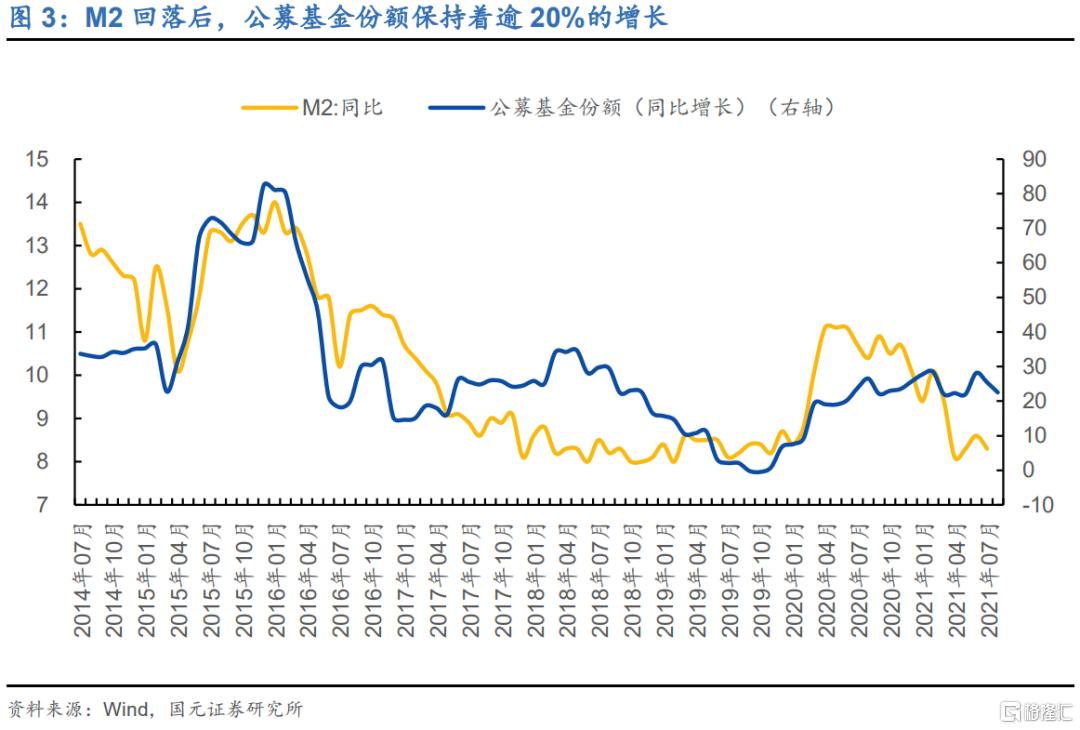

1)天生偏好交易長債的非銀機構的負債端出現了大幅擴張。銀行與非銀機構之間存在不同的期限品種偏好,銀行債券配置偏好短債,非銀機構則偏好持有長債。當前非常明顯的是:資金正在進一步向廣義基金集中,畢竟我們看到在M2這一輪迴落之後,公募基金份額還保持着逾20%的增長。

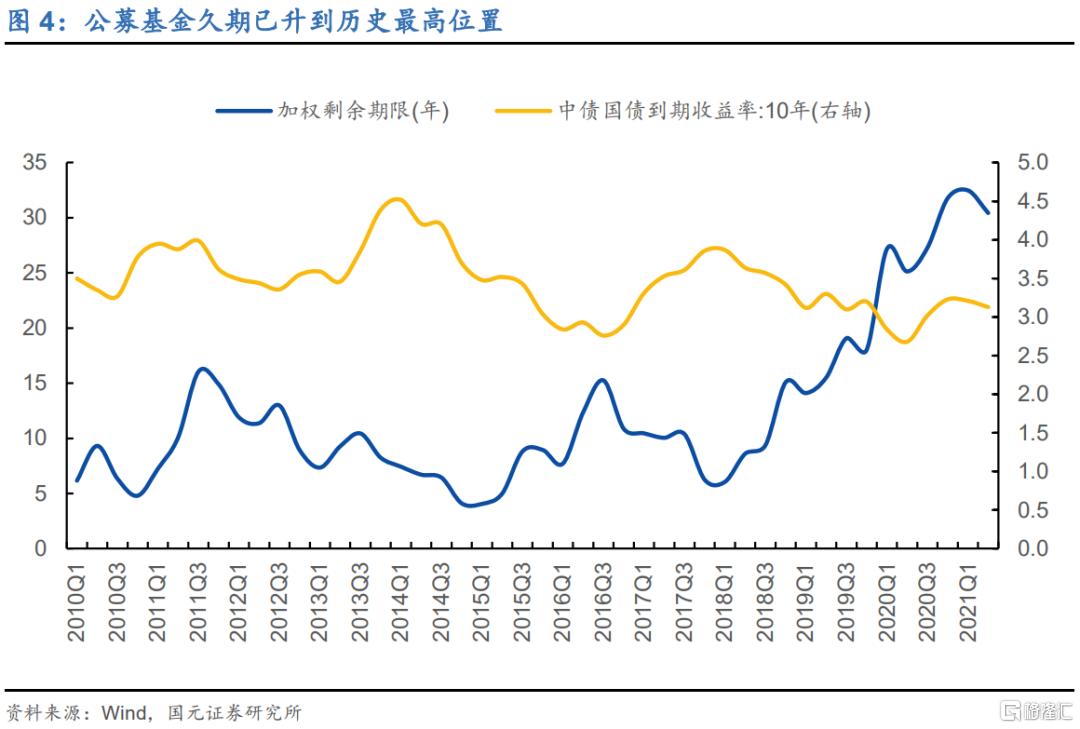

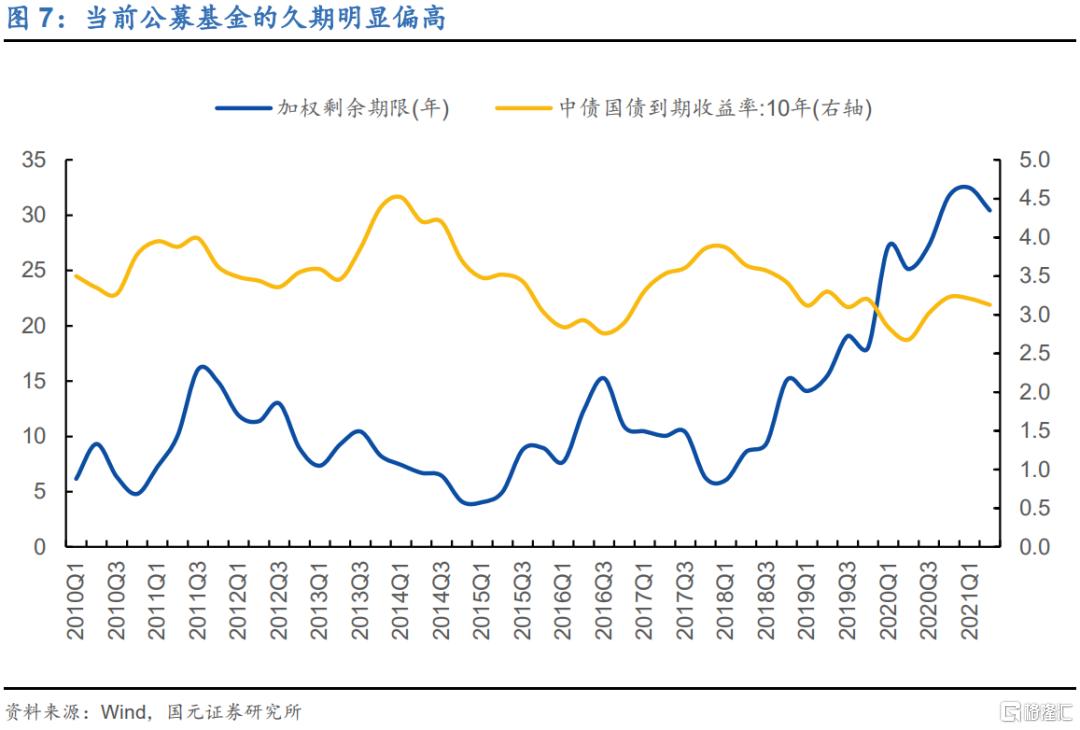

2)當然,廣義基金可能也在積極加久期。歷史上,在每一輪利率的下行階段,公募基金的久期都會相應增加,而當前公募基金的久期不但還在持續上升,而且已經升到了歷史最高的位置(4.5Y),比2016年因委外而大幅加槓桿時的久期狀態還要高。

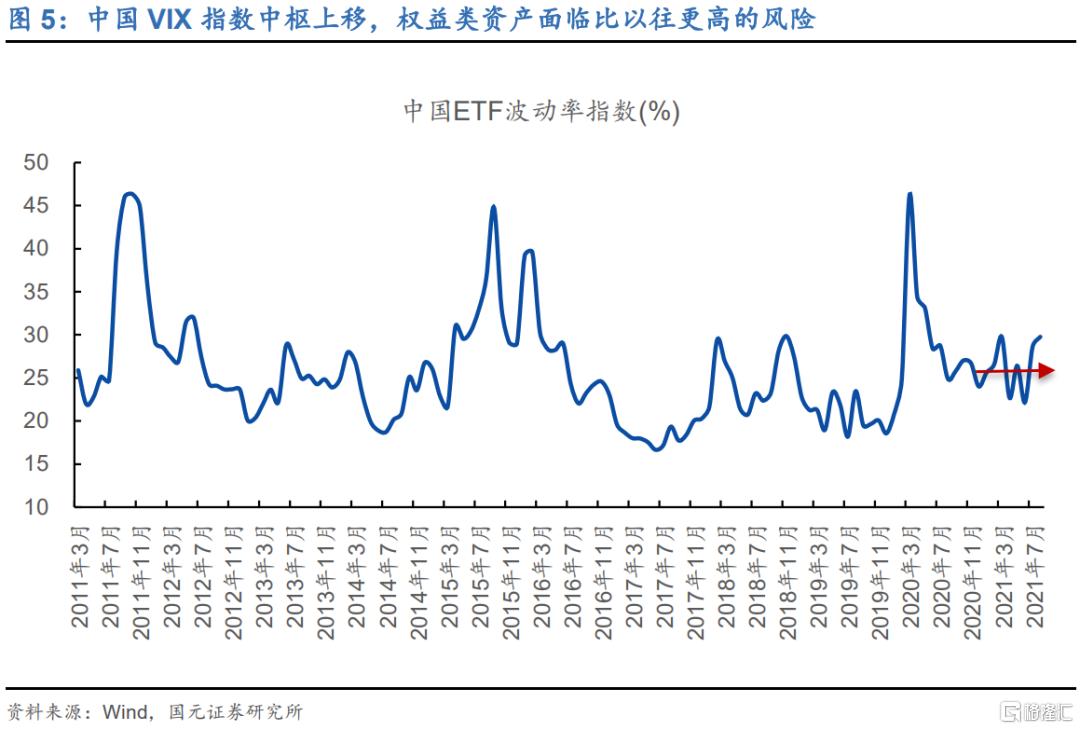

我們猜測,無論在哪個層面,資金被擠向長債資產的緣由是資產荒,這與2016年的環境非常相似。首先,在地產及基建的產業政策層層約束下,有很多資金進不到實體層面之中,只能進入阻力更小的金融市場;其二,權益資產這類中高風險資產的確在今年面臨着比以往更高的風險,中國VIX指數的中樞其實是擡升的,因此,廣義基金中更大比例的資金只能在長端債券上尋找一些相對合適的風險收益比。

但無論是何種原因,這種交易結構本身就意味着利率債的風險。

1)市場過多交易長端債券本身就意味着行情的不穩定。真正可持續的債券牛市必須在貨幣寬鬆的環境下,由短端帶着整個收益率曲線往下走,而如果在存量資金的環境之下,單單從長端把整個曲線往下壓的話,則非常容易形成一個擁擠的交易通道,一旦這個彈簧被壓到接近極致的狀態,閃崩隨時可能發生。

這種閃崩在歷史上曾經發生過兩次,在閃崩之前都出現了長端債券交易過度的現象。一次是2016年10月,當時在長端收益率的交易高增的狀態下,利率出現了急轉;另一次則是在2020年4月,在新冠肺炎蔓延的恐慌之下,市場資金極大程度地做多長端債券,而後行情反轉。

2)公募基金的超長久期也意味着行情的空間已經非常有限。歷史上,公募基金的久期是跟着行情走的,而當前,比起具體的收益率位置來說,公募基金的久期要明顯偏高,這意味着:公募基金對收益率的預期比現實的行情要樂觀很多。那麼,一旦後續的預期出現一些風吹草動,公募基金可能會出現一輪相對劇烈地去久期。

我們要警惕利率這個資產之錨出現意外飆升,大類資產的risk-off趨勢尚未坐實。全球的基本面並未出現非常明顯的下降,加之利率被明顯低估的事實,在這一環境之下,利率其實是易上難下的。如果利率出現預期之外的上升,不但意味着利率債的風險還將延續,也意味着中高風險資產在明年的表現可能要比預期情形更弱一些。

More Content