机构:中信证券

评级:增持

目标价:75 港元

2020 年盈利受损超预期,潜在风险有望一次性释放。预期 2021 年交付强劲,低基数下业绩高增长确定性强。疫情之下,公司在全球飞机租赁商(含融资租赁)排名由 2019 年的第 8 名上升至第 6 名。长期看有望更大程度分享未来行业复苏周期。下调 2020-22 年业绩预测,仍维持“增持”评级。

▍事项:2021 年 1 月 4 日,中银航空租赁发布盈利预警,称由于坏账准备和减值损失,预计 2020 年净利润将较 2019 年下降 25%-30%。2021 年 1 月 6 日,中银航空租赁发布 2020 年第四季度及年度营运数据。

▍2020 年盈利受损超预期,潜在风险有望一次性释放。根据公告,中银航空租赁2020 年归母净利润预计在 4.92-5.27 亿美元之间,低于我们此前预计的 5.89 亿美元,盈利受损超预期。此前我们已提示的 NAS 投资亏损、飞机减值及亚航 X潜在损失风险有望得到一次性释放。具体包括:1)公司疫情期间因债务重组持有的 NAS 股权公允价值亏损将在年内体现,我们测算该项投资亏损约 7000-8000 万美元。2)预计飞机减值及信贷坏账拨备计提超过我们之前预期。海外疫情态势持续恶化,航司经营承压,延迟支付租金回收压力较大,且可能出现二轮延迟现象。另一方面,疫情反复致使需求修复推迟,Max 复飞加剧供给过剩,从中期看减值不可避免(特别是此前较 A320 存在溢价的 B737NG 系列和宽体机型)。叠加中小航司破产和重组带来的市场供应增加,减值压力进一步加大。3)亚航 X 已提交债务重组计划,预计该潜在损失也将在年报中体现。

▍由于 2020 年交付不及预期,预计 2021 年交付强劲,低基数下业绩高增长确定性强。根据公告,中银航空租赁 2020Q4 完成 25 架飞机交付,2020 年全年完成 54 架飞机交付,低于此前预期的 70 架。预计主要由于 12 月海外、特别是欧洲疫情恶化超预期,线下交付遇阻,使得 2020 年 12 月仅交付 16 架。根据公司交付计划,2021 年计划订单簿交付 37 架,售后回租 17 架,加计延迟交付16 架,2021 年计划交付数将达到 70 架。订单簿中所有计划于 2023 年前交付的飞机均已提前锁定航司客户;2020 年全年飞机利用率 99.6%,自有飞机仅一架脱租,但已承诺租赁,业绩可预见性较强。而 2020 年 46%飞机交付于第四季度,其中 30%于 12 月交付,这意味着新飞机创造的收益将主要体现在 2021年。尽管 2021 年飞机市场价值仍存在进一步走低风险,但考虑 2020 年低基数,2021 年利润预计将迎来高确定性大幅增长。

▍关注全球疫苗落地进程,耐心等待实质性拐点出现。根据 IATA 数据,2020 年 前 10 个月 RPKs 较 2019 年下降 65%,而与航空需求最直接相关的是政府的旅行限制措施。不仅国际客运需求在跨境限制下恢复路途漫漫,国内市场需求也受到旅行限制趋严和旅客信心下降的影响,飞机交付进度由于物理隔离也被迫延期。大规模接种疫苗是放开边境管制,行业出现实质性拐点的先决条件。截 至 2021 年 1 月 6 日,全球已有 35 个国家开始接种,累计共接种超过 1500 万剂疫苗。全球已有 14 只疫苗进入 3 期临床,有 9 只疫苗在不同国家获得不同程度的授权使用。我们预期拐点后将迎盈利与估值双升,建议投资者左侧布局,耐心等待收获期。

▍长期显著受益于行业景气复苏后供需缺口扩大和租赁渗透率提升带来的行业红利。1)行业层面看,我们再次强调自 2020 年年中以来的观点,老旧飞机加速退役以及供应商减产均将加大未来供需缺口,即使需求恢复后航司也将更倾向于使用停飞中的最新机型或优先安排新交付的飞机。租赁渗透率随着售后回租交易活跃正在上升,航空周期的拐点随着有效疫苗落地而日益明确。新一轮周期起点已然确立,且随着全面复苏时点的不断推后,其未来反弹空间和确定性在不断增加。2)后疫情时代,公司在资产端、客户端、资金端均具有明显优势,有望更多享有行业复苏红利。中银航空租赁公司合理利用困境,通过积极的售后回租策略实现逆势扩张,在全球飞机租赁商(含融资租赁)排名由 2019 年的第 8 名上升至第 6 名。同时机队依然保持年轻,平均机龄 3.5 年,平均剩余租 期 8.6 年,资产端优势明显。2020 年末服务客户收窄至 87 家大中型优质航司客户。依托中国银行大股东支持与自身 A-的信用评级,2020 年末可动用流动资金超过 50 亿美元。

▍风险因素。全球疫情扩散及持续时间超预期;疫苗落地及推广不及预期;飞机大幅减值;部分客户发生风险事件。

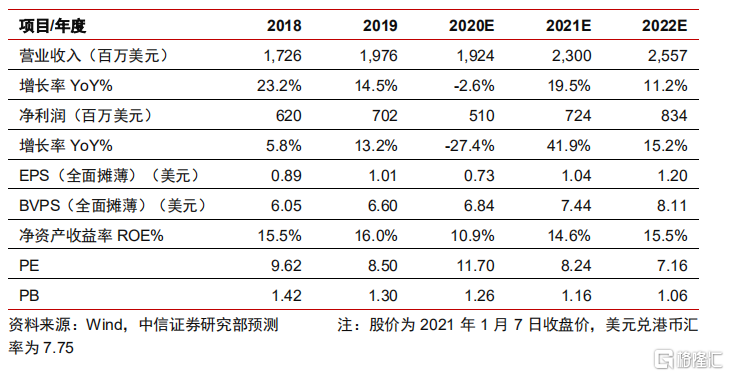

▍投资建议:短期盈利受损,长期分享竞争地位提升和行业景气复苏,维持“增持”评级。考虑亚航 X 债务重组潜在亏损,并调整减值及拨备测算,下调公司2020/2021/2022 年 EPS 预测至 0.73/1.04/1.20 美元(前预测值 0.85/1.15/1.28美元),预计 2020-22 年 BVPS 分别为 6.84/7.44/8.11 美元,现价对应 PB 估值分别为 1.26/1.16/1.06x。给予 2021 年 1.3xPB,目标价 75 港元,维持“增持”评级。

More Content