解读土地出让金政策:“房住不炒”顶层设计进一步成型

本文来自格隆汇专栏:兴证宏观王涵,作者:王涵、王连庆、卓泓

投资要点

2021年6月4日,财政部宣布拟将国有土地使用权出让收入等四项政府非税收入划转税务部门征收,2021年7月1日起7省市试点,2022年1月1日起全面实施;对此我们的看法:

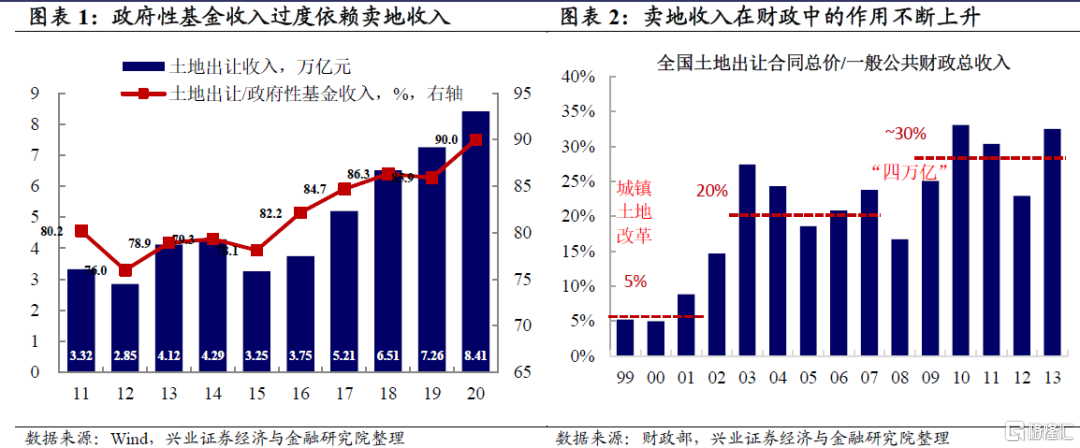

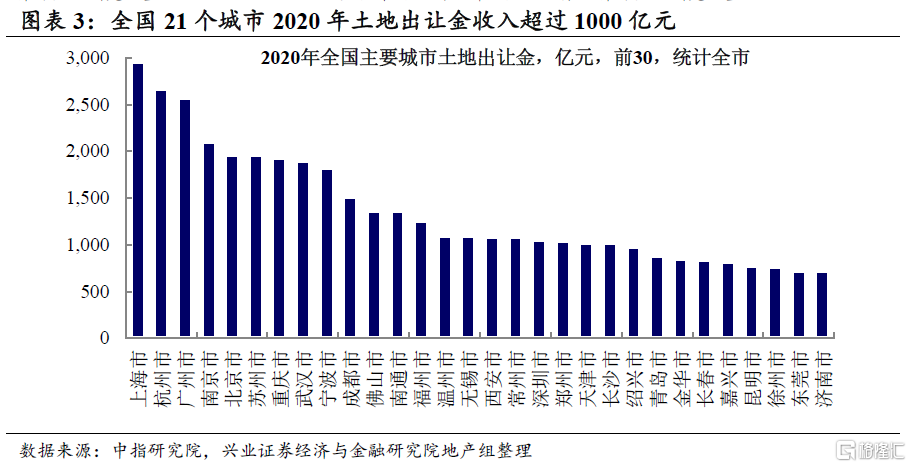

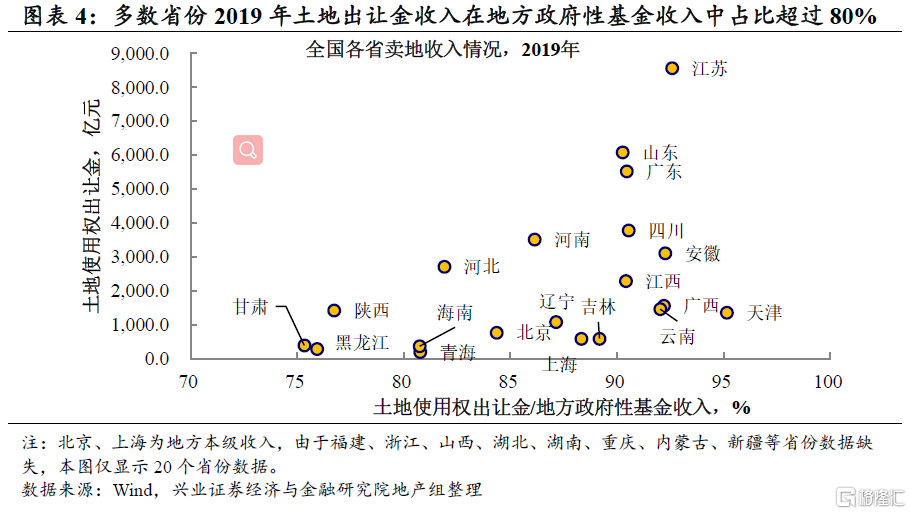

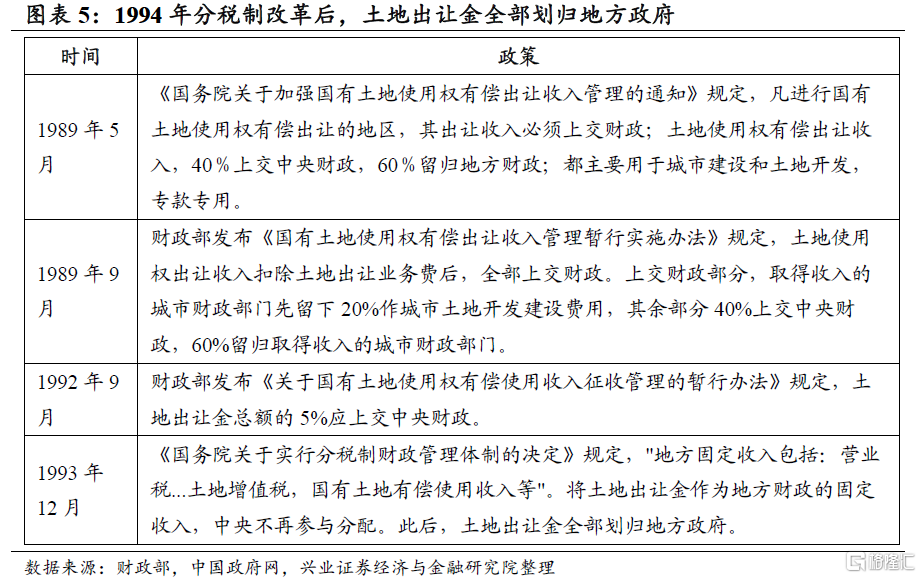

改革背景:分税制改革后,地方财政对卖地收入的依赖持续提升。1994年分税制改革后,国有土地出让收入全部划归地方。彼时,卖地收入在财政收入中占比也很很低。而近年来(尤其是“四万亿”之后),地方财政对卖地收入的依赖持续提升。2020年,土地出让收入8.4万亿,占政府性基金收入90%,占地方政府性基金本级收入93.6%。2021年预算草案的报告中对2021年国有土地出让收入的预算仍高达8.4万亿。

释放信号:中国经济转型下,“房住不炒”顶层设计进一步成型。正如我们在2020年中期报告《先为不可胜》中指出的,在百年未有之大变局的背景下,内循环的意义进一步提升。但是,过高的住房相关支出成为约束内需释放的因素之一,高房价对于将高素质人才留在更具创新能力的城市也是不利的。本次土地出让金划转的改革,体现“房住不炒”的导向下,顶层设计对房地产市场的调控在进一步成型。

主要内容:前期系列财税改革政策延续,通知改变征收但未涉及分配。实际上,本次通知是对包括2018年十九届三中全会、2020年9月,中办、国办土地出让收益使用规定等财政税收改革系列政策的延续。本次通知将土地出让金征收任务划归各地税务局,旨在提升提高效率和规范。关注到本次通知里并未涉及不涉及资金使用分成问题,根据各方报道来看*,土地出让金具体的分配、管理权或仍归于地方财政部门所有。

潜在影响:有助于防范化解存量债务风险,需关注后续政策配套情况。如前所述,土地出让金征收权划归税务部门,增加了顶层设计对土地出让金收入情况的了解,有助于进一步防范化解地方存量债务风险。由于本通知或暂时并不影响地方对土地收入的管理,其对地产投资短期来看影响或暂时有限。但往后,地方拿地动力是否会受影响、其重心是否会从卖新地转向旧城改造,及其对地产投资的可能影响,需要持续关注。此外,考虑到此前卖地收入在地方财政的重要性,需要关注后期是否会有相应的财税政策配套推出。结合5月11日财政部等四部委召开地产税改革试点的工作座谈会,需要持续关注地产税等政策的后续发展。

风险提示:土地政策及地产政策调控推进超预期。

风险提示:土地政策及地产政策调控推进超预期。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.