机构:信达证券

评级:买入

本期内容提要

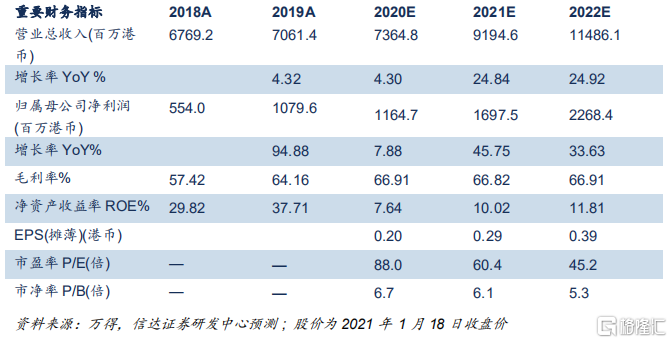

国内洗衣液与洗手液龙头品牌商。公司成立于 1994 年,是洗衣液及洗手液行业龙头品牌商,同时布局厨房卫浴等家居清洁产品;其中洗衣液连续11 年市场第一,19 年市场份额超过 24%,洗手液连续 8 年市场第一,19年市场份额超过 17%,家居清洁尚在培育期,市占率排名第五,19 年市场份额为 1.7%。2020 年 12 月公司港交所上市,实际控制人持股比例超过 75%,股权集中。近年来公司收入平稳增长,归母净利率提升带动业绩高增长,截止 2019 年,公司收入 70.5 亿港币,17-19 年复合增速为12%,归母净利润为 10.8 亿港币,17-19 年复合增速为 254%。

品类升级及新品类普及推动家清行业平稳增长,对标海外集中度品牌商格局有提升空间。根据 Frost&Sulliva 数据,2019 年中国家清行业市场规模为 1108 亿元,15-19 年复合增速为 5%,行业平稳增长;对标美国、日本成熟市场,2019 年中国家清人均支出占比存在一倍以上提升空间。品类升级与新品类普及提升是驱动行业增长重要因素,例如洗衣液占比衣物清洁行业仅 40%,将持续替代洗衣粉,衣物柔顺剂、地板清洁剂等品类逐步普及带来新市场。我国家庭清洁行业品牌商集中度较高,2019 年衣物清洁、家居清洁、个人护理领域 CR3 分别为为 48%、61%、65%,相比于日本、美国发达市场超过 80%的集中度存在提升空间,例如衣物清洁领域日美 CR3 分别为 92%、83%,头部企业有望借助渠道资源、品牌积淀及资金实力进一步提升市场份额。

产品持续创新、重视终端用户运营、流量变化敏锐、信息化前瞻布局为公 司长期稳健发展护航。其一,公司具备扎实研发基础,善于产品创新,为产品持续迭代提供基础,公司 2008 年及 2015 年国内首创洗衣液及浓缩洗衣液,掀起品类升级革命,树立专业化品牌形象;其二,公司注重终端消费者运营,强化品牌心智,自 2009 年加大线下促销人员对消费者对接,2015 年创新 O2O 模式增强与用户沟通,头部品牌中蓝月亮品牌享受溢价;其三,公司流量变化敏锐,线上渗透率超过行业平均水平 15pct;其四,前瞻信息化布局提升产业链运营效率,增强终端洞察,提升渠道管理精细化程度及生产效率,为长期发展奠定基础。

渠道优化及浓缩洗衣液新趋势提升衣物清洁市场地位,加大推新有望打开家居清洁天花板。未来公司将在衣物清洁及手部清洁领域继续深耕,同时补足家居清洁领域短板,具体而言:1)优化渠道布局,加大终端下沉力度,扩展品牌终端触达率:公司近年推出针对分销商的数据系统以及针对终端促销人员管理系统,提升线下分销渠道管理效率;同时进行分销商优化,淘汰合作不佳分销商,加大优质分销商资源开拓,扩大网点下沉深度。 2)浓缩洗衣液方兴未艾,公司作为行业领引者有望借得先机抢占流量: 19 年海外发达市场浓缩洗衣液渗透率超过 90%,中国市场仅 8%,未来提升空间大,公司作为国内浓缩洗衣液标杆,约 28%市场份额,未来有望加大市场培育提升份额。3)加大推新,率先布局家居清洁领域,提升细分市场份额:19 年公司新出 4 款高端产品,重点布局厨房及卫浴领域,有望拉动细分领域增速。

盈利预测与投资评级:我们看好品类升级迭代以及新兴产品渗透率不断提升对产品家庭清洁行业推动作用,行业保持平稳增长,同时蓝月亮作为洗衣液、洗手液等升级品类龙头品牌商,将通过渠道延展优化以及前瞻新品布局提升份额,未来可期。我们预计公司 2020-2022 年收入分别为 74 亿港币、92 亿港币、115 亿港币,同比增速分别为 4%/25%/25%,归母净利润归母净利润分别为 11.65 亿港币、16.98 亿港币、22.68 亿港币,对应增速分别为 8%、46%、34%,根据最新收盘价(2021 年 1 月 18 日)对应 PE 为 88 倍、60 倍、45 倍;根据相对估值法,与化妆品公司相比,公司 PEG 为 3.1 倍,低于可比公司 4.4 倍平均水平;根据绝对估值法,假设公司半显性增速为 15%,永续增速为 1.5%,WACC 为 8.4%,每股合理内在价值为 21.95 港币,存在低估;首次覆盖,给予“买入”评级。

股价催化剂:渠道扩展进度及优化效果好于预期、至尊浓缩洗衣液及其他新品类市场推广效果好于市场预期,衣物清洁行业消费升级进度加快。

风险因素:1)渠道优化及延展不达预期;2)新品销售不达预期;3)原材料成本上涨及费用未能优化进而影响利润率提升;4)市场格局恶化影响份额提升。

More Content