作者:长江宏观固收赵伟团队

来源:长江宏观固收

报告摘要

8月企业盈利重新跌至负增区间,受工业生产销售放缓、PPI跌幅扩大等影响

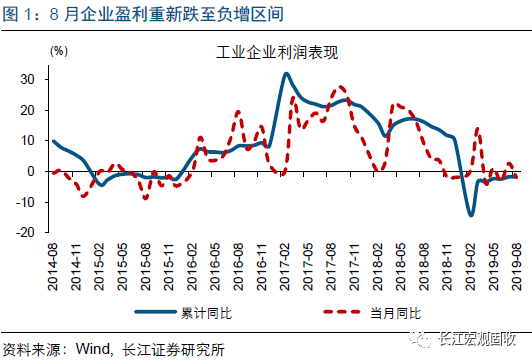

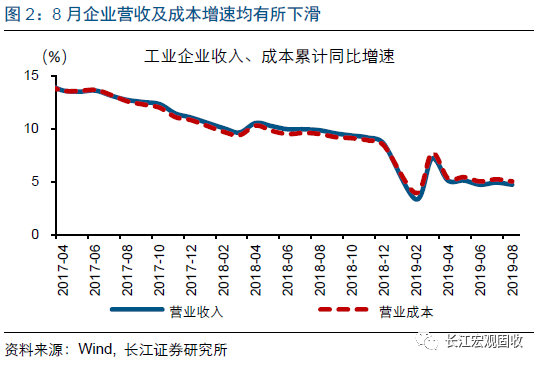

8月企业盈利重新跌至负增区间,亏损企业数量加速增长。8月,规模以上工业企业利润当月同比下滑2%(7月当月同比增长2.6%),重新跌至负增区间;1-8月利润累计同比增速-1.7%,年初以来持续处于负区间。工业企业主要经济效益指标中,企业营业收入1-8月累计同比增长4.7%、较前值下滑0.2个百分点,亏损企业家数69804家,同比增长5.7%,较前值(4.3%)上升1.4个百分点。

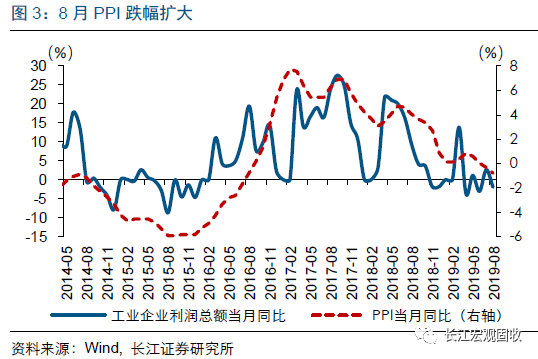

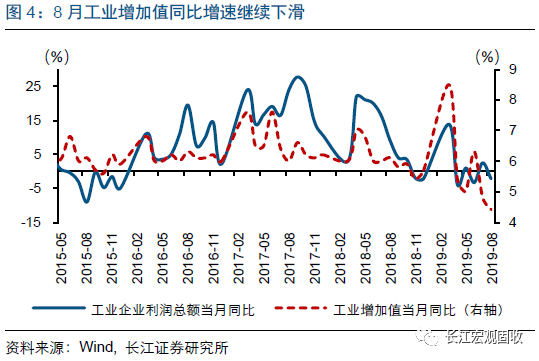

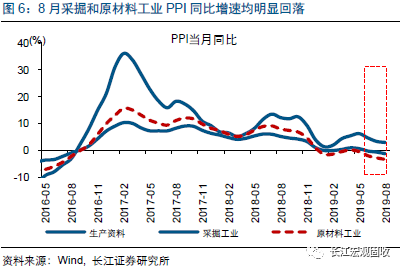

8月盈利增速明显下滑,或受工业生产销售放缓、PPI跌幅扩大等因素影响。8月企业利润总额和营业收入增速下滑,受量、价两个维度因素的共同影响。量的层面,8月工业增加值同比增速4.4%、较前值下滑0.4个百分点,跌至近年单月最低水平;价的层面,8月PPI同比增速-0.8%、较7月跌幅进一步扩大0.5个百分点。此外,8月超强台风等或也对工业企业利润产生一定负面影响。

盈利表现继续分化,上游行业盈利增长放缓,消费制造类制造业盈利多数改善

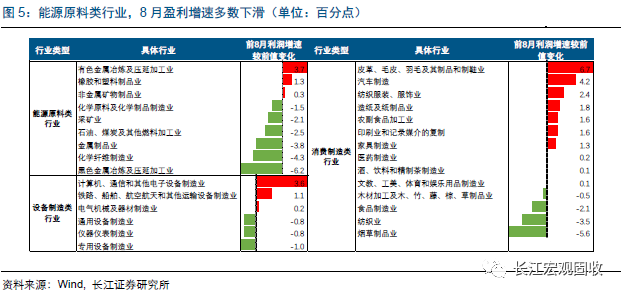

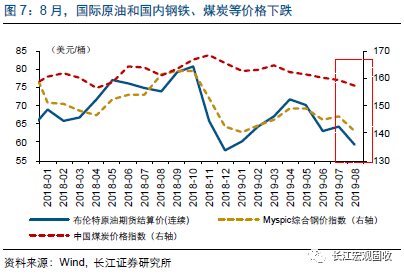

部分中上游行业盈利增速回落幅度较大,或与原料价格下跌等有关;下游消费类行业盈利多数改善。今年8月,全球原油、国内钢价和煤价等下跌,拖累生产资料PPI大幅回落,拖累相关行业利润增速下滑。其中,采矿业1-8月累计利润增速较前值下滑2.1个百分点,黑色加工冶炼跌幅扩大6.2个百分点。部分消费制造类行业、高技术制造业和战略性新兴产业,8月盈利增速有所回升。

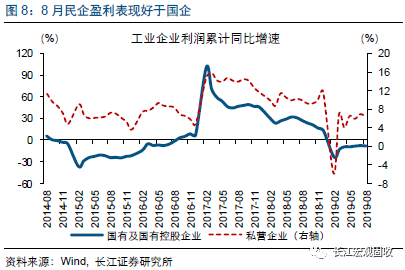

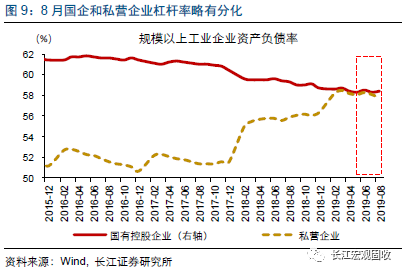

分企业类型来看,民企盈利继续正增长、表现好于国企,小型企业盈利也相对较优。1-8月,国企盈利增速-8.6%、跌幅近一步扩大0.5个百分点,私企盈利增速也有回落,但仍然保持正增长、累计同比6.5%;大中型企业盈利增速-5.3%,明显低于工业企业平均水平,反映小型企业盈利相对较好。杠杆率视角来看,8月国企杠杆率提升0.1个百分点至58.4%,私企下滑0.3个百分点至57.8%。

重申:务必重视“资产荒”的深刻影响;利率债短期仍有扰动,中期利多不变

重申长江宏观观点:务必重视“资产荒”对市场行为的深刻影响。债券市场,短期来看,中美贸易谈判进展、通胀预期变化、地方债潜在供给等,或对债市表现产生阶段性干扰;中期来看,宏观环境、“资产荒”下再配置压力的逐步显现等,依然对债市形成有力支撑。股票市场,投资策略已逐步转向流动性框架。

风险提示:

国内宏观政策或经济基本面出现大幅调整。

报告正文

事件

2019年1-8月,全国规模以上工业企业实现利润总额40163.50亿元,同比下降1.7%、持平前值;8月规模以上工业企业利润总额同比下降2%(前值增长2.6%)。

(数据来源:国家统计局)

点评

8月盈利增速重新跌至负区间,或受工业生产销售增速放缓、PPI跌幅扩大等影响。8月规模以上工业企业利润同比下滑2%,较上月下滑4.6个百分点;1-8月盈利同比下降1.7%,持平前值。主要财务指标中,1-8月企业营业收入累计同比增长4.7%、较前值下滑0.2个百分点。企业利润和营收增速的下滑,受量、价两个维度因素的共同影响;8月工业增加值同比增速4.4%、较前值下滑0.4个百分点,8月PPI同比-0.8%、较7月跌幅进一步扩大0.5个百分点。此外,8月超强台风或也对企业利润产生负面影响。

分行业来看,部分上游行业盈利增速回落幅度较大,或与原料价格下跌等有关;下游消费类行业盈利多数改善。今年8月,全球原油、国内钢价和煤价等有所下跌,拖累生产资料PPI大幅回落,影响企业利润。其中,采矿业累计利润增速下滑2.1个百分点,黑色加工冶炼跌幅扩大6.2个百分点。部分消费相关制造业,8月利润增速有所回升;其中,汽车制造、计算机电子制造,1-8月利润累计同比跌幅分别收窄4.2和3.6个百分点。皮革制品、家具制造利润增速分别上升6.7和1.3个百分点,可能与美国“抢消费”等存在一定关联。先进制造业表现亮眼,1-8月高技术制造业和战略性新兴产业利润分别增长2.8%和3.0%,增速分别较前值加快1.6和0.5个百分点。

分企业类型来看,民企盈利继续正增长、表现好于国企,小型企业盈利也相对较优。1-8月,国企盈利增速下滑0.5个百分点至-8.6%、盈利增速跌幅进一步扩大,仍处于负增长区间;私营企业和小型企业利润同比分别增长6.5%和10.3%,部分受益于下游消费制造业盈利支持。杠杆率视角来看,国企和私营企业表现小幅分化,今年8月国企杠杆率小幅提升0.1个百分点至58.4%,私营企业杠杆率下滑0.3个百分点至57.8%。

重申长江宏观观点:务必重视“资产荒”对市场行为的深刻影响。债券市场,短期或仍有扰动,中期利多逻辑不变。短期来看,中美贸易谈判进展、通胀预期变化、地方债潜在供给等,或对债市表现产生阶段性干扰;中期来看,宏观环境、“资产荒”下再配置压力的逐步显现等,依然对债市形成有力支撑。股票市场,投资策略已转向流动性框架。

More Content