Market NewsHong Kong stocks "open the door green" after the festival! The number of Hang Seng students fell nearly 4%, the Hang Seng Index fell below the 21000 point mark, and technology stocks fell across the board. Consolidation continued?

Market NewsHong Kong stocks "open the door green" after the festival! The number of Hang Seng students fell nearly 4%, the Hang Seng Index fell below the 21000 point mark, and technology stocks fell across the board. Consolidation continued?Hong Kong stocks weakened again after the Easter holiday.

Today, Hong Kong stocks opened low. As of press time, the Hang Seng Technology Index fell nearly 4 per cent to 4150, the State-owned Enterprises Index fell 3.07 per cent to 7158, and the Hang Seng Index fell 2.44 per cent below the 21000-point mark.

All aspects of technology stocks are green. Bilibili is down 10.49%, Baidu-SW is down more than 6%, Meituan is down 5.93%, Alibaba, Kuaishou and Xiaomi are down more than 3%, NetEase, Ctrip and Tencent are down more than 2%.

On the market, inner housing stocks, coal stocks fell collectively, retail, Internet health care, tobacco concept, sporting goods and other concepts fell at the top. On the other hand, electric power stocks, oil stocks, heavy infrastructure stocks, pork stocks and other stocks strengthened.

It is worth noting that China Merchants Bank, which had previously suffered from high-level shocks, fell more than 11% to HK $53, with a latest market capitalization of HK $1.3366 trillion. The company announced last night and agreed to remove Tian Huiyu from the post of president and director of China Merchants Bank. Tian Huiyu has been the third president of China Merchants Bank for nearly nine years. JPMorgan Chase said in a statement that the sudden change in management of China Merchants Bank will not have any impact on the financial position of China Merchants Bank, but the share price is expected to face downward pressure in the short term.

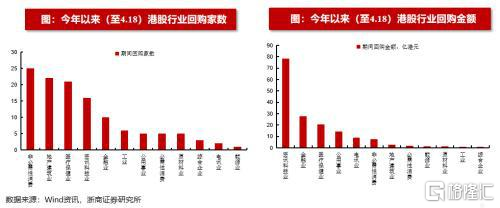

The wave of buybacks hit a new high

What are the factors behind the continued volatility of Hong Kong stocks? A noteworthy point is that the scale of buybacks in the Hong Kong stock market has reached an all-time high.

Zheshang strategy data show that in terms of years, the scale of Hong Kong stock buybacks reached an all-time high in 2021. The total volume of Hong Kong share buybacks reached HK $38.25 billion in 2021, much higher than in 2020 (HK $16.15 billion) and a year-on-year growth rate of 137 per cent.

Since the beginning of this year (to April 18), the scale of Hong Kong stock buybacks has once again shown explosive growth. Since 2022, the amount of Hong Kong share buybacks has reached HK $16.5 billion, far exceeding the level of the same period in previous years and a year-on-year growth rate of 132.9 per cent.

The 20 listed companies with high share buyback scale so far this year are: Tencent Holdings (HK $6.098 billion), AIA (HK $2.677 billion), Xiaomi Group-W (HK $1.208 billion), China Gas (HK $1.11 billion), China Mobile (HK $866 million), Yao Ming Bio (HK $843 million), Sansheng Pharmaceutical (HK $581 million), Ping an good Doctor (HK $246 million), Tianlun Gas (HK $214 million), Minhua Holdings (HK $148 million), Mingyuanyun (HK $137 million), Yi Da (HK $137 million), Skyworth Group (HK $121 million), Popomat (HK $90 million), Kingdee International (HK $88 million), Haohai Biotechnology (HK $0.85 billion), Conch Entrepreneurship (HK $81 million), China Biopharmaceutical (HK $75 million), Liwen Paper (HK $65 million).

What are the signals from the massive wave of buybacks? Some analysts pointed out that historically, the sharp increase in share buybacks may be an effective and practical leading indicator at the bottom of the market in the medium term, and the buyback tide highlights the midline value of Hong Kong stocks.

Haitong Securities previously counted that Hong Kong stocks have experienced five rounds of repurchase waves since 2005. summing up these five rounds of repurchase waves, we can find that at the beginning of the Hong Kong stock buyback wave, the market has often fallen by a large margin, and the valuation has also reached a relatively low level. as the market falls further and valuations fall further, the intensity of buybacks continues to increase. After all the buyback waves, Hong Kong stocks have stabilized and rebounded, and both the Hang Seng Index and Hang Seng Technology can bring better investment returns after the end of the buyback wave in the medium to long term.

How can I get there in the future?

Since last year, the Hong Kong stock market has shown a deep adjustment under the resonance of multiple internal and external uncertainties. According to the recent research and judgment of the comprehensive market, the Hong Kong stock market still maintains a range of shocks in the short term.

Domestically, the number of confirmed outbreaks continues to rise and the resulting supply chain and logistics disruptions add to market concerns about future growth prospects, according to CICC's strategy. In addition, geopolitical tensions continued to superimpose hawkish signals from Fed officials, pushing interest rates on 10-year Treasuries to a high of 2.84 per cent, causing spreads between China and the US to hang upside down for the first time since 2010. The upside-down has raised concerns among investors about capital outflows and devaluation pressure on the renminbi, as well as whether it will restrain policy loosening.

However, those concerns were partly allayed by subsequent signals from the State Council and the subsequent RRR cut announced by the central bank on Friday, suggesting that steady growth remains a core concern for policy makers. However, it may also be inevitable that the external environment brings some constraints to the policy deployment. Therefore, in the current stage, fiscal and other industry growth policies should be relayed and further strengthened.If various challenges at home and abroad are still likely to continue for some time, further efforts to stabilize growth are still necessary and urgently needed.

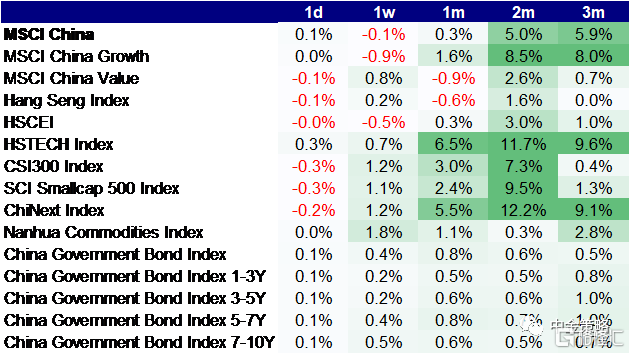

From a historical point of view, overseas Chinese capital stock markets usually have a positive performance after the reserve cut.

Source: Wande Information, China International Capital Corporation Research Department

Zhang Jintao, a Castrol fund, explained the reasons for the upside-down interest rate spreads between China and the United States and the future market trend, saying that the interest rate spread between China and the United States is only a disturbing factor, and the most important thing at present is to control the epidemic, stabilize the economy, and wait for enterprises to make profits. the market still has more investment opportunities. In overseas markets, if the Fed moves very quickly to raise interest rates, coupled with a shrinking table, it may put some pressure on the US capital market, which may have some impact on Hong Kong A shares, but this impact is not the main contradiction. Hong Kong A shares still rely on their own fundamentals.

Hong Kong stocks are offshore market, mainly institutional investors, trading volume is low, turnover rate is also relatively low, so the valuation is also low. Is it a value depression or a value trap for Hong Kong stocks? Zhang Jintao believes that, first of all, it must be a value depression, but whether it is a value trap depends on the fundamentals of individual stocks and the whole. From an investment point of view, priority should be given to those stocks that not only have low valuations, but also whose fundamentals are upward in order to make money for the growth of corporate profits and enjoy dividends at the same time.

Haitong International Wang Shengzu previously said that the bottom of Hong Kong stocks may have appeared, but the rebound is not strong enough, the market needs a long time to repair, should not have a big rebound or reversal expectations. After all, the capacity of the Hong Kong stock market is not as large as that of the mainland and the United States. The increase in interest rates in the United States will also lead to capital outflow from Hong Kong. The outflow of capital from Hong Kong will not be offset by the northward flow of water to the south. In the face of the economic slowdown and the epidemic, the mainland economy is expected to improve in the second half of the year, so the Chinese and Hong Kong stock markets are expected to show a trend of high after low for the whole year.

CICC said it expected that Hong Kong stocks were still likely to maintain relative consolidation in the recent uncertain macroeconomic environment. Some key variables that will affect the market trend in the future include: 1) the progress of Sino-US regulatory cooperation and the easing of geopolitical tensions; 2) changes in the domestic epidemic and its impact on economic growth; and 3) the strength of stable growth politburo quarterly economic situation analysis meeting in mid-late April, for example, the signal significance is more critical. On the whole, the opportunities faced by the market in the medium term still outweigh the risks, and further policy support is expected to boost market sentiment. Compared with A shares, the advantage of Hong Kong stocks is that the valuation level is significantly lower and the dividend yield is relatively high. Specific to the plate allocation, in the environment of market fluctuations and sluggish economic growth, the target of high dividend yield and high-quality growth stocks with large pre-adjustment will provide investors with more protection in the recent market fluctuations.

More Content