【中泰宏观】全球经济金融高频数据跟踪:欧洲服务业再走弱

作者:中泰宏观研究团队

来源:梁中华宏观研究

经济状况:

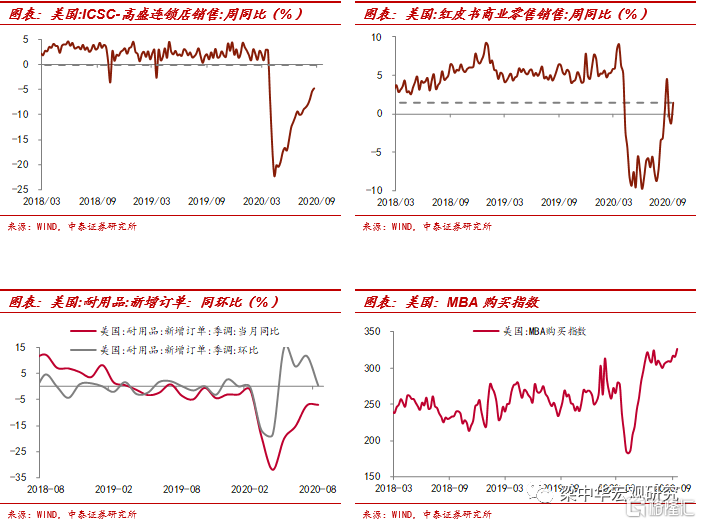

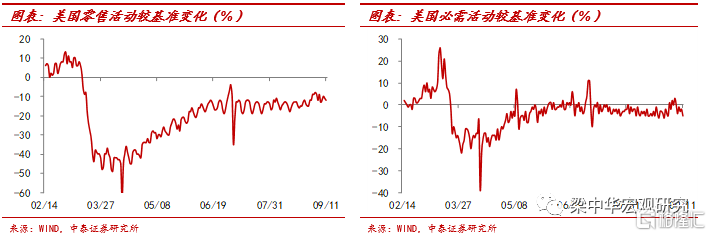

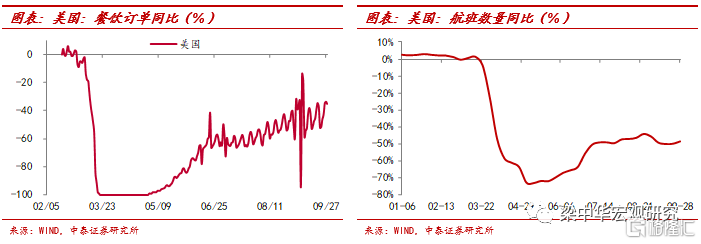

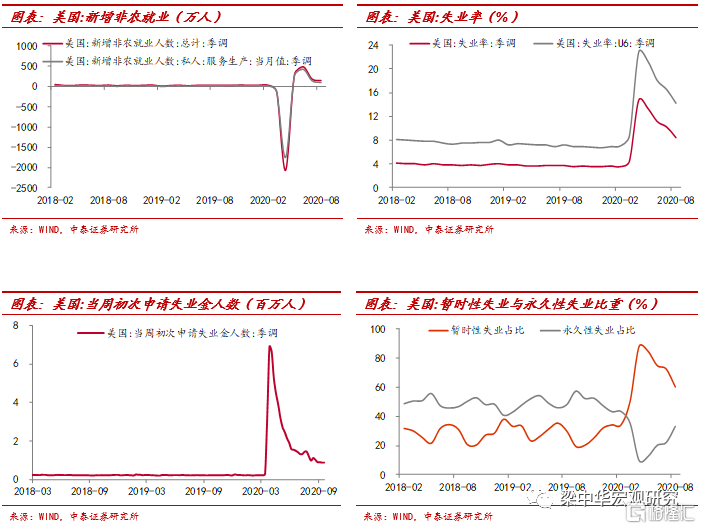

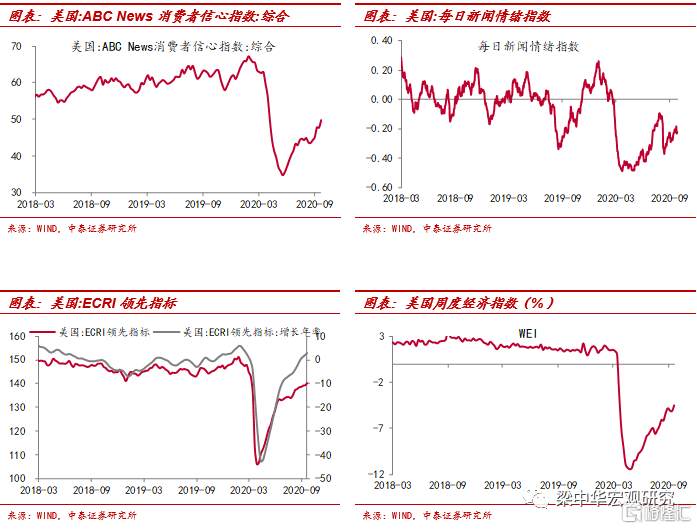

美国:本周红皮书商业零售销售同比转涨至1.5%;航班量较去年同期仍下滑48.6%;消费者信心指数回升至49.8,新闻情绪指数则回落至-0.22%左右;截止9月19日,初请失业金人数仍高达87万;截止9月24日,周度经济指数回升至-4.5%。

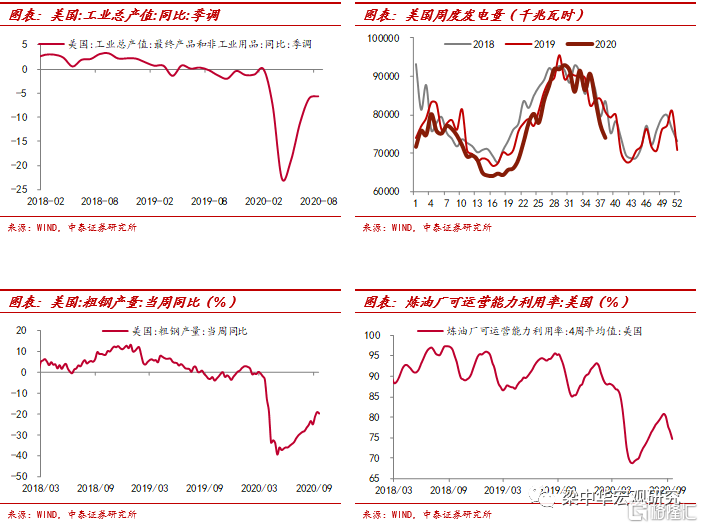

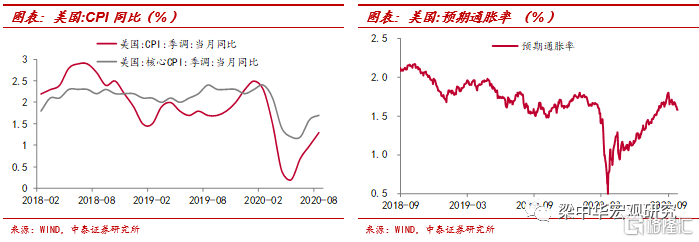

8月美国耐用品订单同比小幅回升至-7.1%,环比仅0.5%,不及预期,较上月大幅放缓;8月成屋销售环比增长2.4%,是2006年底以来最大月度增幅,主要得益于利率的持续下行;截止9月18日,周度发电量较去年同期下滑8.4%,跌幅4月以来新高;截止9月25日,美国预期通胀率回落至1.58%。

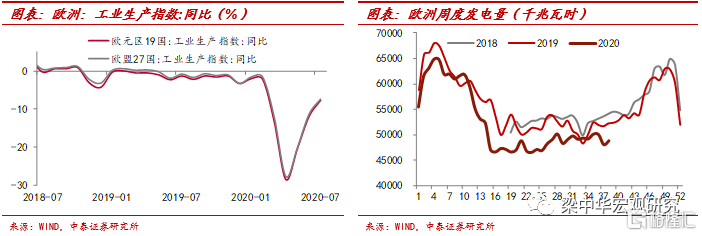

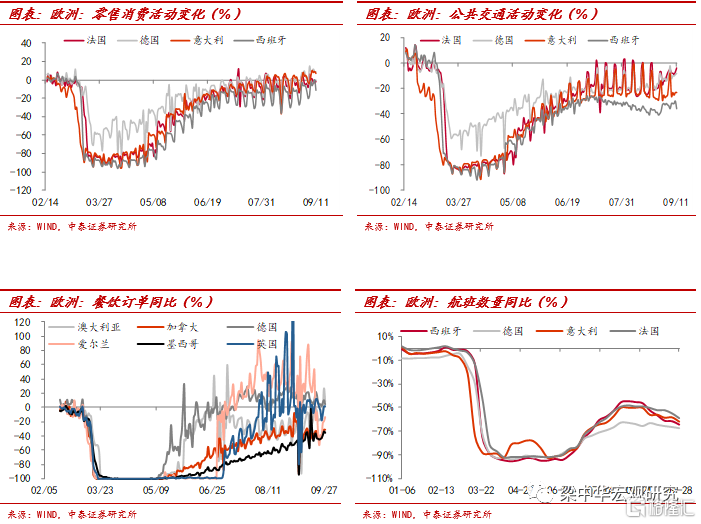

欧洲:本周欧洲主要国家消费活动有所回落,如德国餐饮订单恢复度较上周下滑约6个百分点;加拿大餐饮订单较基期跌幅扩大至-35%。就航班量来看,欧洲多数国家跌幅仍在6成左右。此外,截止9月18日,欧洲周度发电量较去年同期下滑6.5%。

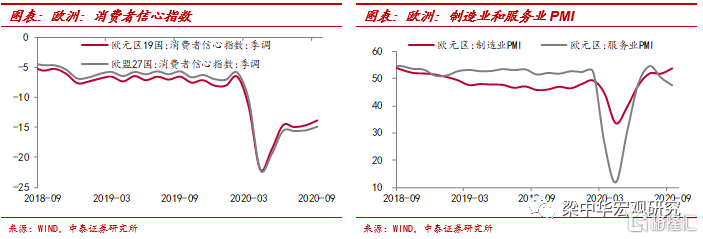

8月欧元区消费者信心指数小幅回升至-13.9%;8月制造业PMI指数再度回升至53.7,但服务业PMI指数再度下滑至枯荣线以下,主要是受二次疫情冲击影响。

金融状况:

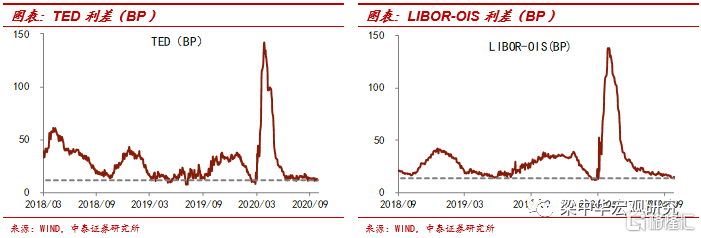

流动性:TED利差和LIBOR-OIS利差指数维持在正常水平,流动性暂无危险。

央行:本周美联储、欧央行和日央行等仍在持续宽松,截止9月26日,美联储总资产为7.09万亿美元,欧央行和日央行则扩表至6.5万亿欧元和689.69万亿日元。

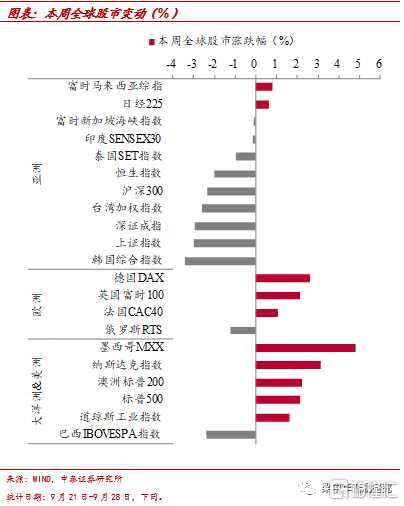

股市:本周亚洲股市多数下跌,欧美股市多数上涨。韩国和中国跌幅靠前,韩国跌幅超过3%,上涨指数跌幅也接近3%。墨西哥涨幅最大为4.8%,其次为纳斯达克上涨了3.1%,德国和英国涨幅也超过2个百分点。

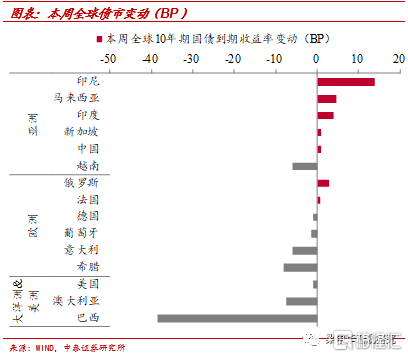

债市:本周国债收益率多数下行。欧美多数国家10年期国债收益率在下行,尤其是巴西下行了38.6个BP,希腊、意大利以及澳大利亚下行幅度也超过5BP。亚洲多数国家国债收益率在上行,尤其是印尼上行了14个BP,中国上行0.9个BP。

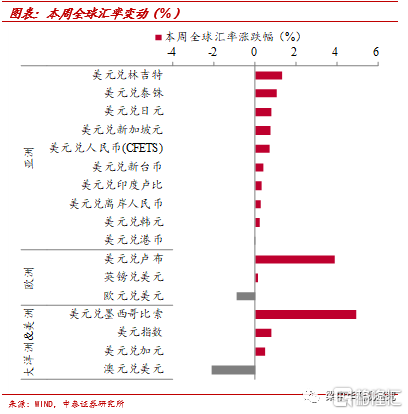

汇率:本周美元指数续升,多数国家相对贬值,英镑则相对升值。人民币离岸价继续贬值,美元兑人民币离岸价从21号的6.79小幅回升到28号的6.81。

商品:本周原油大幅下跌,其中INE原油价格跌幅超过5%;贵金属以及黑色商品继续下跌,COMEX白银跌幅超过11%,SHFE白银跌幅超过17%,DCE铁矿石跌幅超过4%。

疫情状况:

美洲:美洲每日新增病例小幅抬升,近一周平均每日新增病例超过4万人;巴西每日新增病例则相对稳定,近一周平均每日新增病例不到3万人。

欧洲:欧洲疫情仍在爆发,尤其是西班牙每日新增病例高达3.2万人,继续创历史新高;法国也比较严重,每日新增病例超过1万人;英国每日新增病例则接近第一次爆发时期。鉴于欧洲疫情二次爆发态势明显,多个国家的防控措施再度加强,或对经济恢复产生一定影响。

亚洲:日本每日新增病例在逐步回落,而印度每日新增病例在放缓,但依旧相当严峻,最近一周平均每日新增病例仍高达8.3万人。

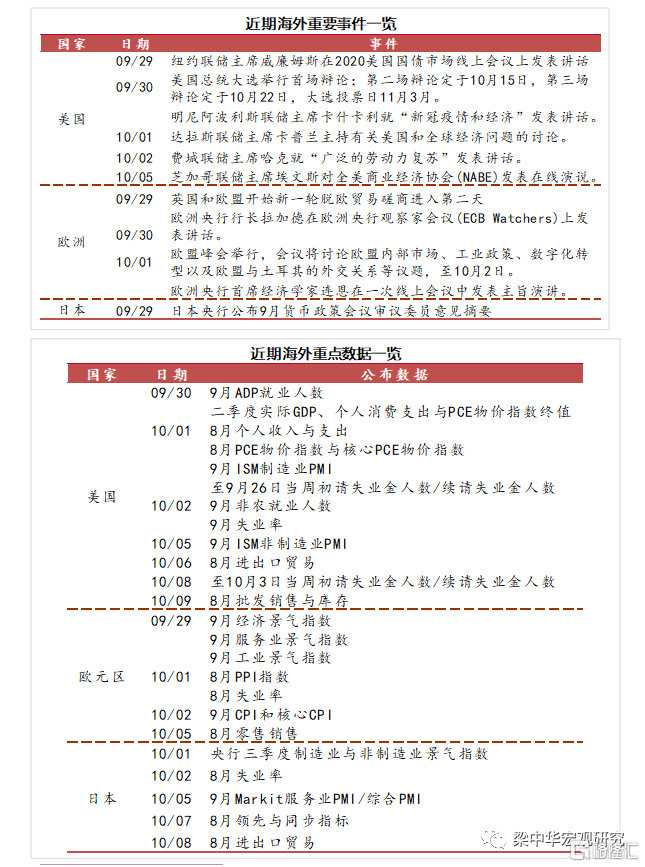

双节假期,海外应该关注那些事?

下面列出了部分高频数据图表,详细目录可参考文末,如需详细数据库,可联系本团队成员。

美国经济状况

1、美国生产

2、美国需求

3、美国就业

4、美国景气

5、美国通胀

欧洲经济状况

1、欧洲生产

2、欧洲需求

3、欧洲景气

4、欧洲通胀

全球市场状况

1、美元流动性

2、全球股市

3、全球债市

4、全球汇率

4、全球商品

全球疫情状况

1、每日新增

详细目录

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.