机构:中信证券

评级:买入

目标价:172.80 港元

公司 2020H1 实现营收 188.6 亿元,同比+21.1%;净利润 17.8 亿元,同比+24%;毛利率同比+1.1pct 至 19.5%,净利率同比+0.2pct 至 9.4%。尽管疫情影响下产能利用率下降以及研发费用增加导致成本费用提升,公司上半年业绩表现仍然强劲。展望未来,随手机镜头数量和规格的不断升级以及车载业务的持续放量,我们持续看好公司发展前景,维持“买入”评级。

▍公司上半年营收及净利润同比+21.1%/+24%,疫情下业绩表现仍然强劲。公司2020 上半年实现营收 188.6 亿元,同比+21.1%;净利润 17.8 亿元,同比+24.0%;毛利率同比+1.1pct 至 19.5%,净利率同比+0.2pct 至 9.4%。公司上半年营收增长主要受益于智能手机业务发展持续向好.尽管疫情影响下镜头业务产能利用率降低带来毛利率下滑,以及研发投入带来费用提升,公司上半年净利润仍有超20%同比增长。费用端来看,公司上半年销售/研发/行政费用分别同比+4%/+29.2%/+29.5%,销售/研发/行政费用率分别同比-0.1pct/+0.4pct /+0.1pct至 0.7%/5.7%/1.8%。研发费用增长较快,主要源于公司持续投放资金于高规格产品,推动产品结构升级,而行政费用增长主要系防疫相关费用投入。展望未来,疫情影响持续减弱下,随手机镜头数量和规格的不断升级以及车载业务的持续放量,我们持续看好公司未来发展前景。

▍分部而言,疫情影响下镜头业务毛利率有所下滑;内部改造初显成效,模组毛利率超预期提升。(1)光学零件业务:手机镜头上半年出货 6.45 亿颗,同比+16.5%,其中 6P 及以上镜头占比达 24.6%,车载镜头出货 2050.6 万颗,同比-8.7%,仍保持了全球第一的领先地位。镜头业务上半年营收达 38.64 亿元,同比+2.4%,毛利率同比-2.6pcts 至 41.5%,主要系疫情影响下终端厂商出货递延及欧洲车厂停产导致产能利用率降低,且上半年手机光学规格升级不及预期,高端产品需求拉动不足。下半年,随疫情影响持续减弱,预计终端客户订单量有望逐步恢复。随公司产品结构持续升级及产能利用率的逐步回升,我们预计公司镜头出货量将继续提升,毛利率有望维持;手机镜头和车载镜头全年出货量将分别增长 10%和 5%。(2)光电产品业务:CCM 上半年出货 2.68 亿颗,同比+25%,营收约 148.7 亿元,同比+27.3%。其中高规格的潜望式和大像面模组上半年出货 3219.3 万件,同比+200%;毛利率同比+5.2pcts 至 11.1%,毛利率大幅改善主要受益于公司生产流程的优化和 CCM 产线自动化的改造,下半年随公司出货结构持续改善,毛利率有望维持。我们预计公司 CCM 全年出货量将增长 10%。(3)光学仪器业务:上半年实现营收 1.26 亿元,同比+3.9%,毛利率为 38.6%,同比-2.6pcts,系疫情影响导致产能利用率下降,下半年随疫情影响减弱毛利率有望恢复。

▍展望未来,中长期看镜头与模组数量及规格的升级仍将是公司成长主线。上半年疫情影响下,光学行业规格降级,影响公司镜头和模组产品的 ASP(我们估算公司手机/车载镜头上半年的平均 ASP 大致在 4.33/36.8 元,2019H1 大致为4.88/41.59 元),手机摄像模组上半年的平均 ASP 大致在 54.62 元(2019H1 大致为 54.42 元))。但在疫情影响持续减弱的趋势下,中长期来看镜头与模组数量及规格的升级仍将是公司成长主线。虽然 2020H1 受新冠疫情影响终端需求承压,但我们认为随手机镜头数量和规格的不断升级以及车载业。

▍务的持续放量,公司未来仍有较好的发展前景。手机镜头方面,目前公司产品规格随客户持续升级,超大像面、10 倍光学变焦、超小头部等镜头按计划成功研发与量产。疫情影响减弱背景下,国际大客户订单量持续恢复,我们认为镜头出货有望持续放量。车载方面,公司已获得应用于主流自动驾驶平台的 8MP 镜头的量产许可;随终端客户需求逐步回暖,产能利用率将回升,我们认为公司仍将受益于车载摄像头领域持续发展、车载成像领域及 ADAS 的快速成长。手机摄像模组方面,公司积极布局高规格模组产品,一亿像素大像面模组、10 倍光学变焦模组均已量产,潜望式及大像面模组的出货量快速提升;未来随模组产品市场的不断放量及公司产品结构的持续改善,我们持续看好公司模组业务的成长。

▍风险因素:海外疫情反复;多摄/3D Sensing/潜望渗透缓慢;ADAS 发展缓慢;模组毛利率下行;大客户销量短期承压;行业竞争加剧。

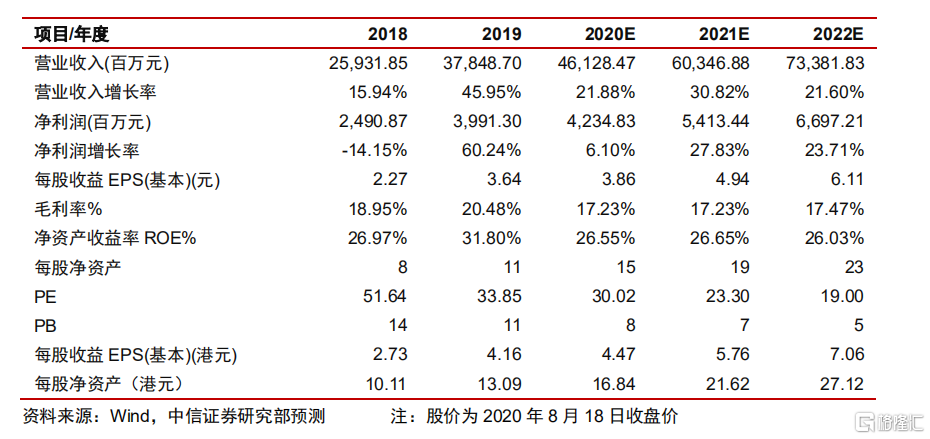

▍投资建议:公司为中国光学龙头,有望持续受益手机光学创新升级及汽车 ADAS 系统加速渗透,多摄/3D/车载等长期成长逻辑明确。我们维持公司 2020/21/22 年 EPS 预测3.86/4.94/6.11 元(折合 4.47/5.76/7.06 港元),考虑公司龙头地位及行业可持续,给予21 年 30 倍 PE,对应目标价 172.80 港元,维持“买入”评级。

More Content