美团点评股价再次来到69港元发行价附近,Q1超预期的财报有效提振了股价,Q2财报即将于北京时间8月23日公布,业绩交流会将于同日19:00召开。

市场密切关注美团外卖利润情况、市占率变化,以及新业务能否持续减亏,若财报表现靓丽,叠加被纳入港股通的预期,或许能成为股价进一步上涨的催化剂。

一、摘要

1、外卖业务经调整经营利润有望在Q2转正;

2、摩拜涨价,打车推聚合模式,新业务19年有望减亏一半;

3、根据万得一致预期,分析师一致目标价为74.66港元。

二、上季回顾:营收同比增长强劲,减亏幅度超预期

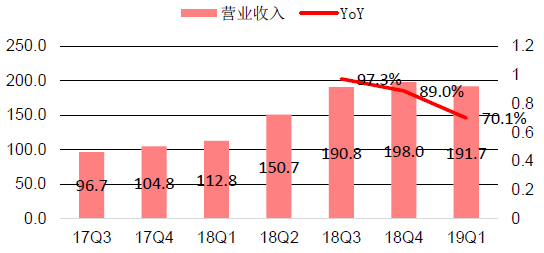

美团点评于5月23日公布了Q1财报,当季营收191.7亿元,同比增长70%,超出市场预期的182.5亿元。Q1交易金额1384亿元,同比提高28%,环比持平。

美团点评季度营收(亿元)及同比增速

来源:中信建投证券

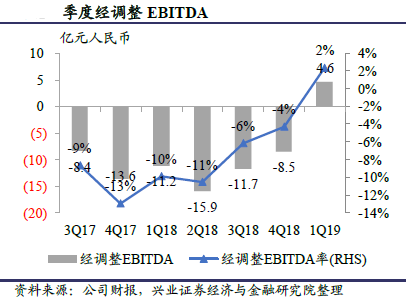

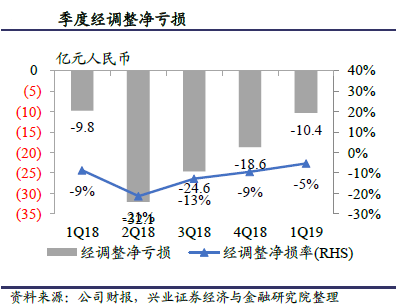

Q1经调整EBITDA为4.59亿元,首次由负转正。Q1经调整净亏损10.4亿元,连续三个季度收窄,也少于市场预期的亏损17亿元。主要是由于摩拜出行业务亏损缩窄以及用户激励减少。

可以说美团点评Q1交出了一份满意的成绩单,公布财报后的第一个交易日股价上涨4.9%,截至8月21日,累计上涨18%。那Q2业绩还会惊喜不断吗?股价进一步上涨的催化剂又在哪里?

三、当季看点

1、外卖:市场最关注什么时候能赚钱

从交易金额和营收来看,外卖都是美团点评的第一大业务,2018年分别为2828亿,381亿,占比分别达到55%,58%。根据光大证券的测算,外卖单均盈利每增加1元,公司整体EPS将增加1.46元。可见外卖业务的盈利弹性巨大,所以何时扭亏成为市场共同关注的话题。

1)外卖业务收入中90%以上来自用户和商家支付的佣金,所以收入可以简单拆分为:

交易用户数×人均交易笔数×每单均价×佣金抽成率

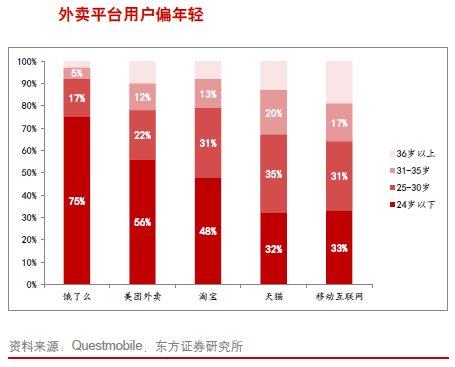

从用户数来看,截至2018年底,餐饮外卖活跃用户数约4.1亿人,约为淘宝的40%,相对来说外卖渗透率仍然较低。根据Questmobile数据,美团、饿了么在24岁以下用户的渗透率远高于淘宝和移动互联网平均水平,25-36岁之间用户的渗透潜力巨大。

人均交易笔数的提升空间也比较大,2018年美团外卖每位交易用户年均交易23.8笔,但头部10%用户年均交易高达98笔。

每单均价提升空间较窄,2016-2018年分别为37元、42元、45元,增速不断放缓。

佣金率未来还能进一步提高,2016-2018年由8.9%提高到13%,未来可能达到14%-15%。

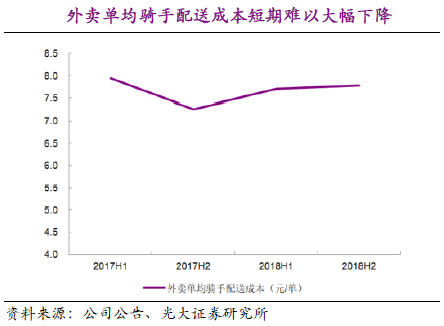

2)成本方面,90%以上产生于骑手,2018年骑手成本为每单7.5-8元,但是每天送单量不到20单,运力远未饱和,未来订单密度的提升是配送成本下降的关键因素。不过外卖订单集中在午晚餐高峰时段,要想大幅提高订单密度有点困难,但是非高峰时段的订单需求挖掘潜力很大。

5月8日,美团宣布开放配送平台,并推出新品牌“美团配送”,目前已与家乐福、CFB集团、百果园、多点、叮当快药达成合作。2018年美团骑手有60万,若运力达到满额状态,成本可以有效摊薄。兴业证券预计,Q2给骑手的高温补贴等较少,单均配送成本有望从Q1的7.9元下降到Q2的7.3元。

3)费用主要是对用户的补贴,目前用户习惯已形成,行业竞争缓和,激励费用占交易金额的比例从16年的4.5%下降到18年的1.9%。

所以整体来看,收入将进一步提升,成本和费用有压缩空间,外卖业务利润改善是非常值得期待的,兴业证券预测外卖业务经调整经营利润有望在Q2转正。

2、新业务:摩拜涨价,打车推聚合模式,亏损会改善吗?

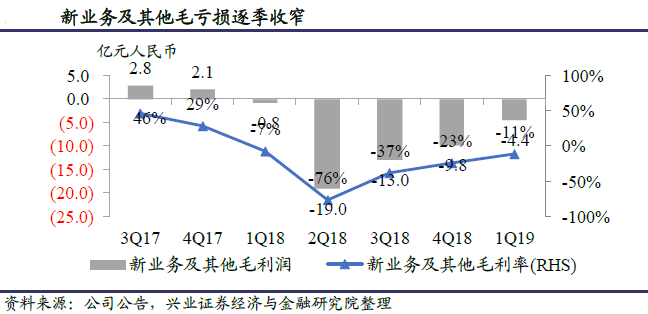

18年美团收购摩拜及进入网约车业务,导致新业务亏损加剧。摩拜单车真的值得收购吗?答案是肯定的,出行是生活服务的重要场景,可以提升用户对平台的粘性,与其他业务产生协同效应。可喜的是,新业务亏损连续三个季度收窄。

摩拜在4月和5月提价,补贴也逐渐减少,未来亏损可以进一步有效缩窄。

而美团打车在4月率先推出聚合模式,向神州、首汽、曹操等第三方平台基于打车金额收取佣金,新模式可以解决司机运力不足,平台高成本、用户需求无法满足等一些列问题,大大提升用户的打车体验。18年美团仅在上海和南京试点网约车业务,司机成本却高达44亿元。未来随着新模式在更多城市的铺开,出行业务减亏可期。

兴业证券预计随着摩拜大规模折旧完成以及聚合模式的推行,美团19年新业务有望减亏一半。

四、分析师预期及评级

根据万得一致预期,分析师对美团点评的一致目标价为74.66港元,其中最高看到95港元。有9位分析师给出“买入”评级,13位分析师评级为“推荐”,2位分析师评级为“持有”。

资料来源:Wind

资料来源:Wind

More Content